The Best Way to Allocate your Stocks in 2022!

Investing in the stock market can initially seem intimidating, but it doesn't have to be. Most of us grew up believing we should leave investing to the professionals, but the truth is you can take control of your finances by understanding these two fundamental concepts.

Investing in the stock market can initially seem intimidating, but it doesn't have to be. Most of us grew up believing we should leave investing to the professionals, but the truth is you can take control of your finances by understanding these two fundamental concepts.

After reading this post you'll have everything you need for getting started with investment, and will be well on your way to choosing how to allocate your stocks in 2022!

And best of all: once you get these down, you'll empower yourself to not only understand how to better allocate your assets, but many other aspects of investing for years to come.

Before we get started, you must be prepared to do your own research. Any investments you make need to match your individual objectives and if you're unsure about choosing your own investments, then a Financial Adviser can help.

This post should definitely NOT be considered as financial advice, however you can book a FREE consultation with a Qualified Financial Adviser please email at admin@riverheadfinancial.co.uk.

How to Allocate Your Portfolio

Diversification is the key to an investor's long term success. The allocation of your assets should be based on two fundamental concepts; your investment objectives and tolerance to risk. You also need to prepare for various economic outcomes as the world around us is constantly shifting.

Allocation is one of the most important concepts in investing. It’s the method by which investors determine how their portfolio will be divided into different asset classes like stocks, bonds, cash, and real estate.

1. Investment Objectives

Investment objectives are determined by your capital requirements in the future. The best place to start is by asking yourself what you're trying to achieve with your investments. Are you saving for retirement? Do you plan on buying a house or car soon? Are you looking to leave money behind for your children when you pass away?

This leads to my next question: when are you likely to need to access the money which you are investing? Since we have no real way of knowing what the future holds, I still recommend setting financial goals so that you are able to move forward. Without these, you’ll find yourself on the sidelines whilst the world around you continues to grow and evolve.

Many investors think they can "time the market" by buying when the price is low and selling when the price is high, but "Asset Allocation: Balancing Financial Risk" by Roger Gibson does a great job of debunking this. He explains that once an investor knows the ideal time they would like to access their money, they can create an optimal strategy by diversifying their investments.

As an investor the key is to stick to your allocation plan through thick and thin. Imagine you have a recipe for a delicious roasted chicken (vegan option also available), which tells you to leave the chicken in the oven for 3 hours but you take it out too early. The chicken will no longer be cooked optimally and the benefits of keeping it in the oven for 3 hours is lost.

Long term strategies are generally safer. Why? Well, historically the market has increased in the long term, however there are sometimes huge corrections which take time to recover from. So as an investor, investing over a long period gives you time to recover from any large dips or crashes.

2. Attitude to Risk

You need to consider that to some degree, you are putting your personality into your portfolio. If you are extremely conservative and risk averse, you should have a portfolio that reflects this. If you are super adventurous and willing to take big risks, then your investments should reflect this too.

Most successful investors buy investments they are comfortable with, rather than what they think will make them rich.

Your psychology when it comes to money is something that has been built over many years with multiple influences. The way your parents raised you, the friends you've had, your career or business experience, and also what kind of leisure you enjoy all shape how you react to investment risk.

Studies generally find that an "emotional" response tends to be much more intense for a loss than for a gain of about the same amount.

This pattern extends not just to money, but also to other things with value, such as possessions or even health. For example, if you were given a placebo pill and told that it would save your life, you'd feel pretty good. But if you were given the same pill and told that it had no medical benefit, you'd probably feel worse than before!

The loss aversion effect can be seen in many financial decisions. One study found that 83 percent of people were willing to pay $3.50 to insure a $2 lottery ticket (a 50% loss aversion), but only 65% were willing to spend $3.50 on a lottery ticket itself (a loss of only 35%). In other words, there's a high degree of risk aversion in investments, even when all else is equal.

The more appetite you have for risk, the more detached you are from the result. This detachment allows investors to take bigger gambles in a hope to make higher returns.

This detachment is often referred to as "risk tolerance," and is one of the most important aspects of an investment plan.

Take this FREE questionnaire to find out your attitude to risk.

My Asset Allocation

Once you've figured out your risk tolerance, you'll be able to decide on an asset allocation. Just remember that your appetite for risk isn't the only thing you need to consider then finalising your asset allocation.

A 22 year old single graduate who is starting their career needs a very different investment strategy to a 50 year old married person who has a number of dependant children.

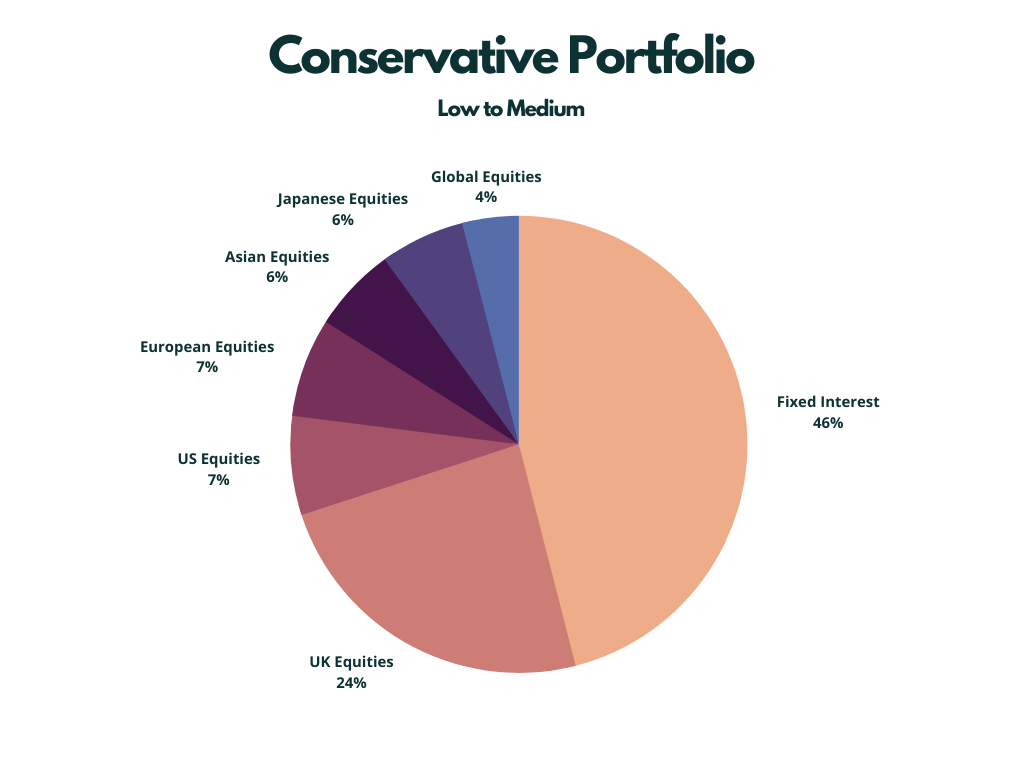

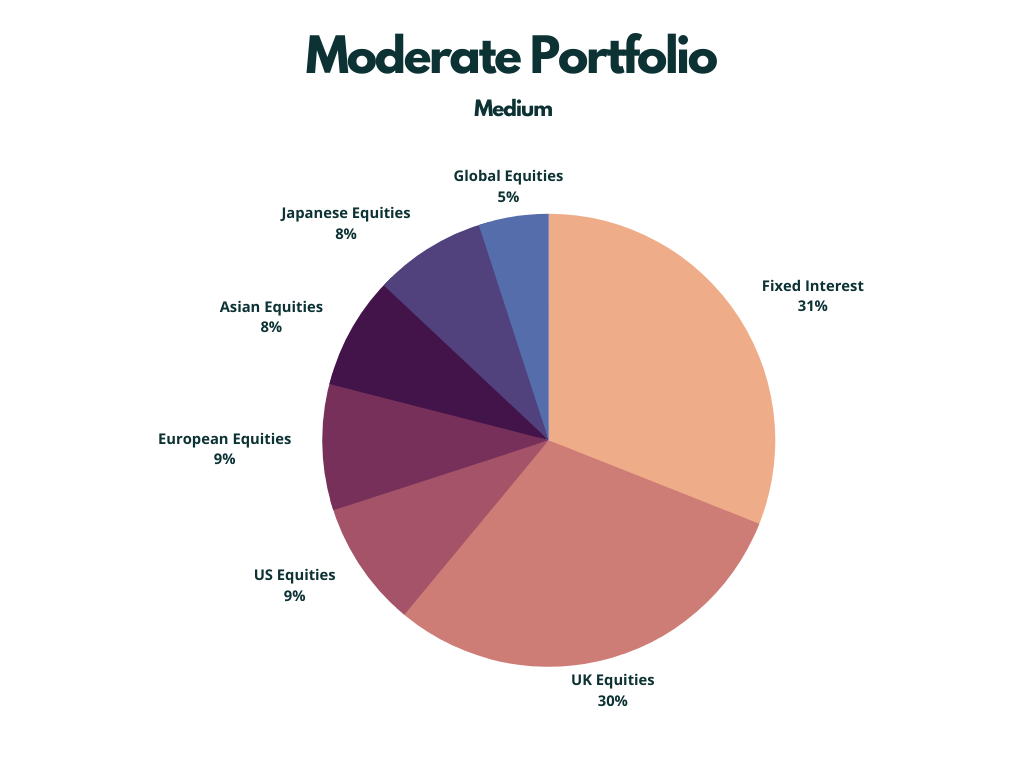

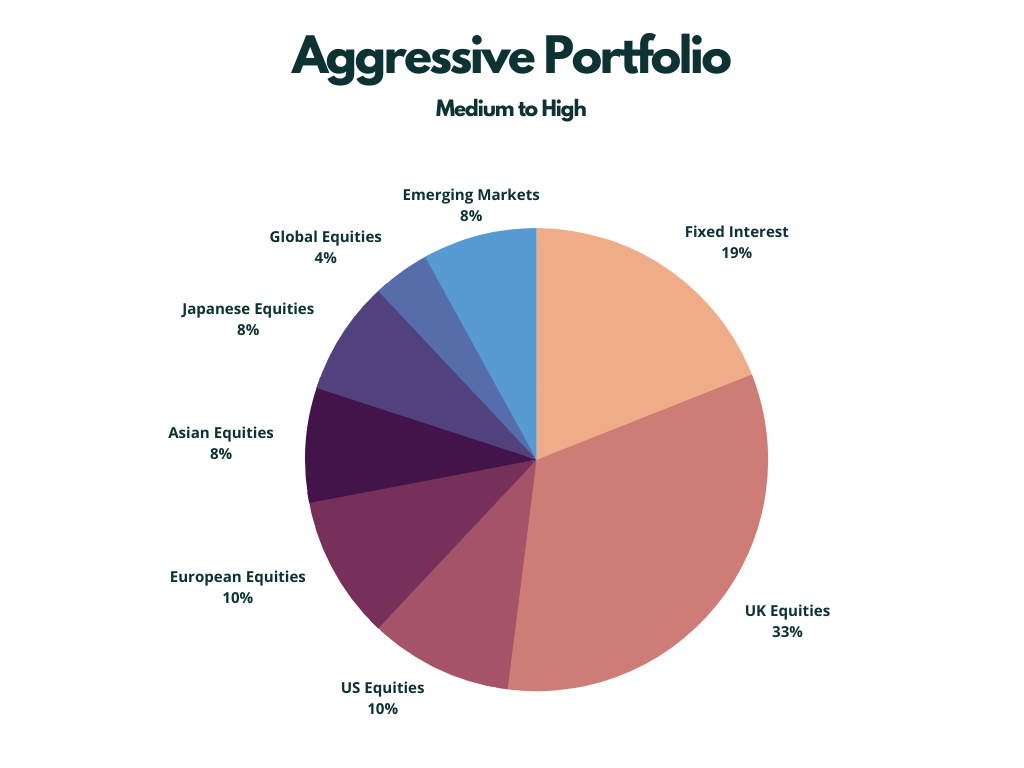

A Financial Adviser can help you with this as they take a holistic view of your entire life when providing any recommendations. However if you are determined to make your own investment decisions, you can find some suggestions for a well diversified asset allocation with a Conservative, Moderate and Aggressive risk tolerance below.

You are free to use these allocations as a reference, and I would recommend you adapt them based on your individual interests. You should have a core strategy for the majority of your capital, but also allow yourself to try new things and take small gambles. Investing doesn't always need to be all uniform and boring!

The main objective of a Conservative portfolio is to preserve the value of your initial capital whilst growing at a rate higher than inflation. This way your savings won't be losing real value each year as prices gradually increase. Investors that are close to retirement tend to switch their portfolios to a more conservative approach in the years leading up to them actually accessing their pensions as they don't want their accounts to take a significant dip right as they stop earning from employment.

Moderate and Aggressive portfolios are for those with more of an appetite for risk. These investors are prepared to sacrifice the protection of their capital in the short term for the likelihood of greater returns in the long term. These portfolios have a majority of the assets weighted to equities. Equities are more volatile than Fixed Interest investments, so can fluctuate dramatically.