Should you buy, lease or finance your next car?

When it comes to getting a new car in 2024, you've got some big decisions to make. Do you buy it all at once, finance it, lease it, or try something like PCP?

When it comes to getting a new car in 2024, you've got some big decisions to make. Do you buy it all at once, finance it, lease it, or try something like PCP? Let's talk about what each of these choices really means in a way that's easy to get.

Prefer to watch? Check out my youtube video instead:

1. Buying Outright

Purchasing a car outright means paying the entire cost upfront. It’s a path of immediate ownership, without monthly payments and interest rates, offering a sense of financial freedom. But this road has its bumps: depreciation hits hard, especially for new cars and luxury brands. A new car can lose about 15% of its value after one year, and close to 50% in just three years. So, while buying outright is probably the simplest option, it's important to consider the long-term costs, and accounting for depreciation.

2. Financing (Higher Purchase)

Financing a car through a hire purchase agreement is like taking out a mortgage. You pay a deposit and then cover the rest in monthly instalments. This path offers the ease of budget management and the joy of driving a more expensive car than your bank account can afford. However, interest rates (starting around 8% for good credit) add to the total cost, and you only reach full ownership after the final payment. Also don’t forget, the car still depreciates. So if you want to sell the car once you’ve paid it off, you won’t get anywhere near as much as you’ve paid over the loan term.

3. Leasing

Leasing is like a long-term car rental. It’s perfect for those who love the feel of a new car every few years. Monthly payments are usually lower, and you don’t have to worry about the car's depreciation or selling it later. But this has its limits - mileage caps and the necessity to maintain the car’s condition. At the end of the lease, you return the car, having paid for its use but with no ownership. This means you’ll need to find a new car all over again.

4. Personal Contract Purchase (PCP)

PCP offers a blend of leasing and financing. You start with an upfront deposit and lower monthly payments, and at the end, you have the choice to pay a final 'balloon' payment to own the car, or return it and start a new deal. It's a route offering flexibility and often lower payments than higher purchase, but the final balloon payment can be a large lump sum, and like leasing, you face charges for excess mileage or damages. It's an option that offers variety, but you need to think about that final choice and its costs.

Let’s compare your options with an example

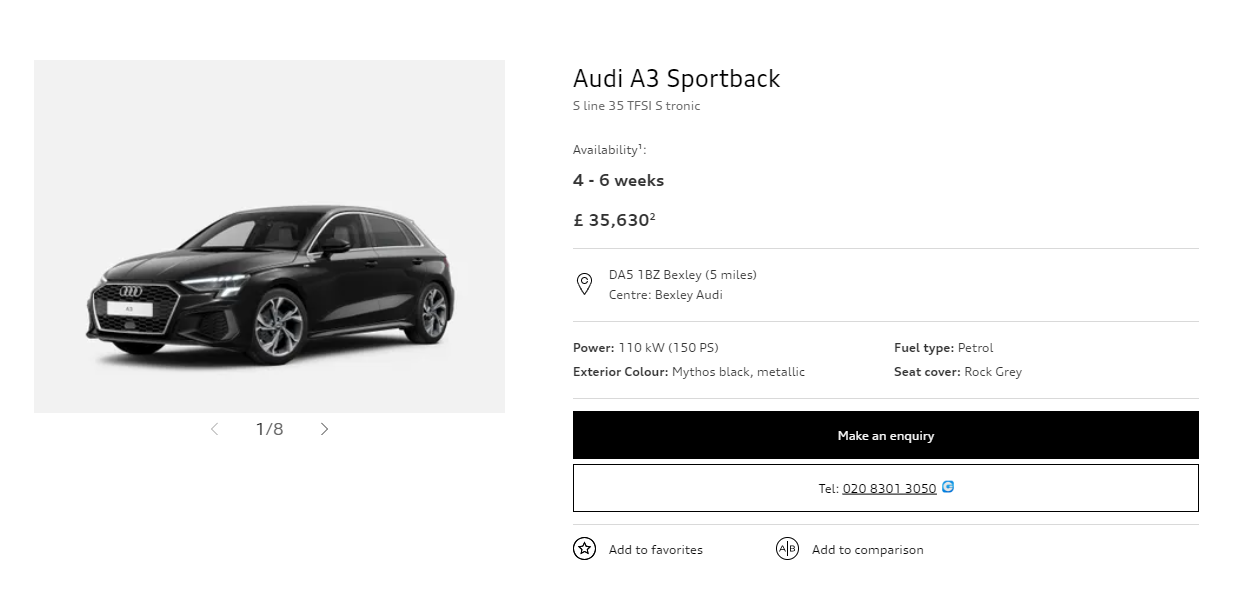

To help paint a clearer picture, let's consider an Audi A3 S line:

Buying Outright

- Cost Now: £35,630

- Cost in 3 Years (after selling for £21,000): £14,630 (considering depreciation)

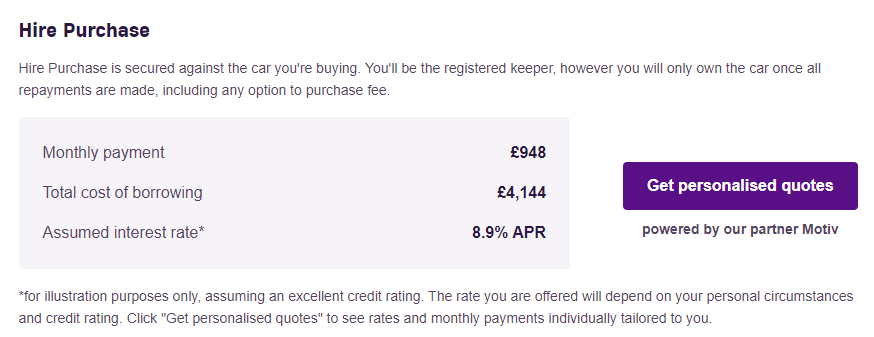

Financing (Hire Purchase)

- Initial Deposit: £6,630

- Monthly Payment: £948

- Total Paid Over 3 Years: £40,774 (including deposit, repayments and interest)

- Cost in 3 Years (after selling for £21,000): £19,774

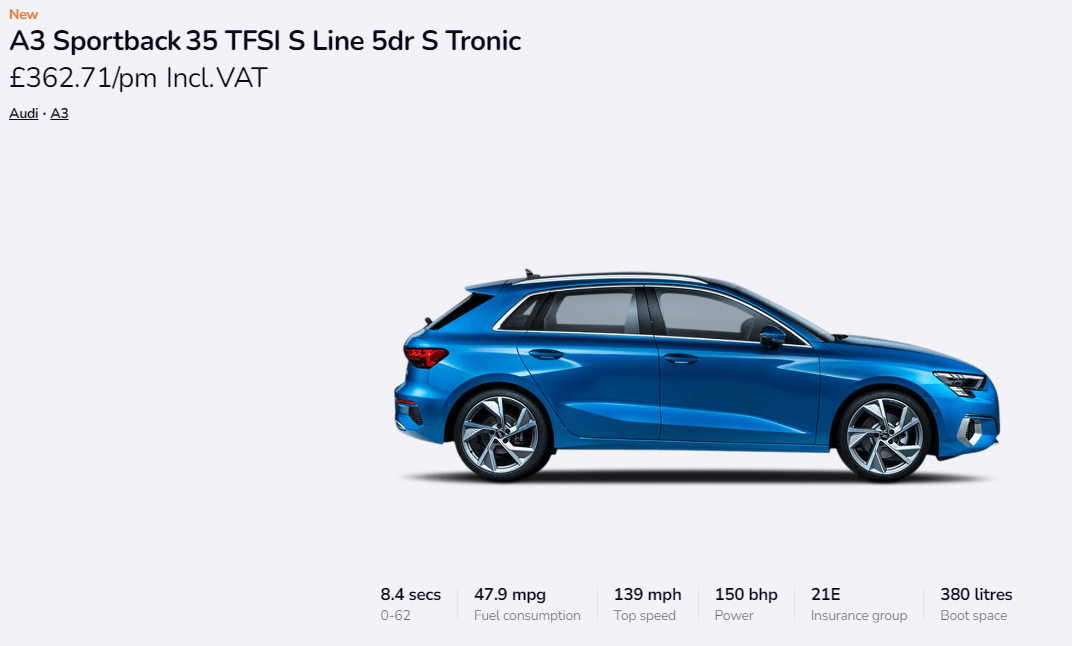

Leasing

- Initial Deposit: £4,302

- Monthly Payment: £362

- Total Paid Over 3 Years: £16,996 (no ownership)

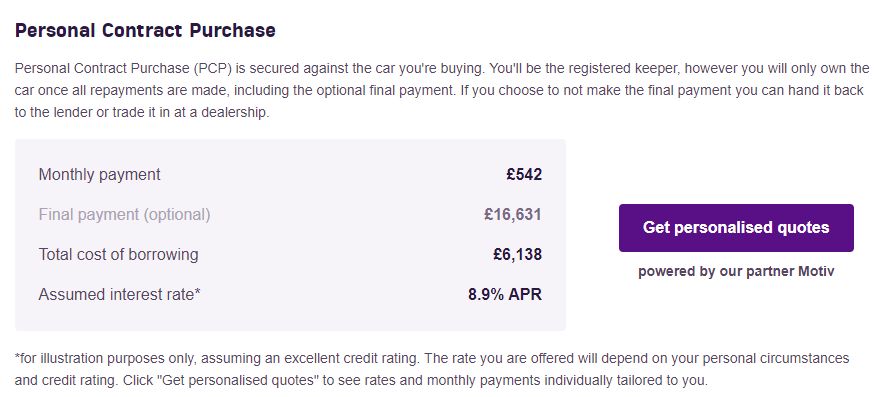

PCP

- Initial Deposit: £6,630

- Monthly Payment: £542

- Total Paid Over 3 Years: £25,600 (without balloon payment)

- Total (if Keeping Car): £42,231 (including balloon payment)

A final comparison

If you decide to buy the car straight up, it's all yours, and it'll cost you around £15,000 over three years. This way, you pay once and don't worry about monthly bills.

If you choose to finance the car, it's a bit more flexible since you don't have to pay everything at once. But in three years, you'll end up paying a bit more, nearly £20,000.

Leasing will cost you a bit less, around £17,000 in total, but you don't get to own the car at the end. It's good for those who like to change cars often.

Then there's PCP. It's flexible because you can choose to buy the car at the end, but it's usually the most expensive option, costing just under £22,000 over three years.

If you do want to keep the car after three years, buying it outright is the cheapest. Financing would cost over £40,000 in total, and PCP would be just over £42,000.

Interestingly, if you lease a car, you might have the option to buy it when the lease is up. For example, if you buy the leased car for £21,000, the total you've spent will be less than £38,000, which can be cheaper than financing or PCP.

Making the choice

When it comes to car ownership, your lifestyle and preferences play crucial roles. If you value long-term ownership and want to avoid continuous payments, buying or financing might be the path for you. But if you prefer driving new models without the hassle of selling and don’t mind not owning the car, leasing could be perfect.

My Personal Experience

When I returned to London from Bali in 2022, the inflated used car market pushed me towards leasing, avoiding overpriced purchases. As the market stabilizes, I’m now considering buying a used car, avoiding the heavy depreciation that new cars face.

If you’re still unsure about which one is the best option for you, feel free to schedule a FREE discovery call.

Enjoying my content? Sign up to my FREE newsletter to keep up to date with all my latest posts!